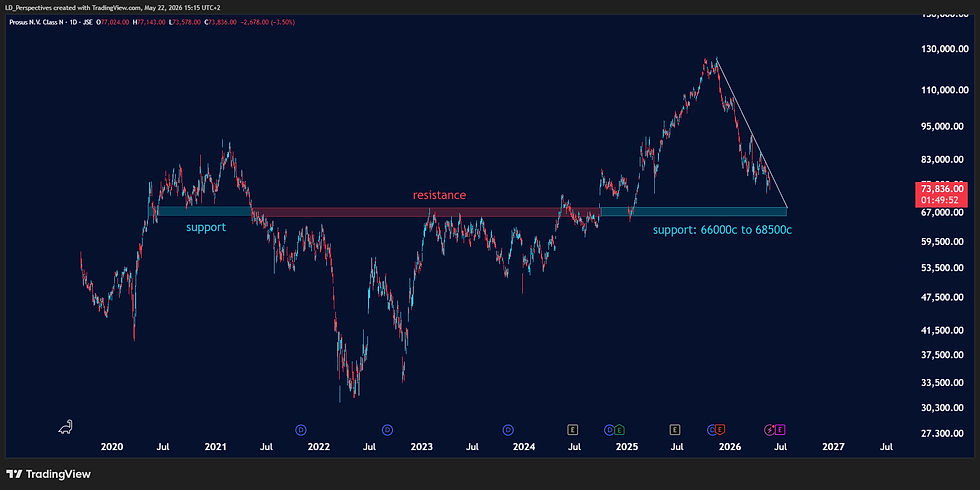

The Narrative of May 2026 Is Defined By A Massive, Synchronized Relative Rotation Where Domestic Financials...

- Lester Davids

- 8 hours ago

- 3 min read

Research Notes May 2026 > https://www.unum.capital/post/rmay2026

Trade Local & Global Financial Markets with Unum Capital.

To get started, email tradingdesk@unum.co.za

NOTE: When Published Intraday, Prices Are Delayed By 15 Minutes

Analysis as of Friday 22 May at 11h09am, prepared for Monday, 25 May.

The narrative of May 2026 is defined by a massive, synchronized relative rotation where domestic financials violently decoupled from the JSE Top 40 to generate severe alpha, funded by the total capitulation of the precious metals spread. By analyzing the momentum regimes entirely through the lens of comparative strength (Sector vs. Top 40), the structural shifts in institutional capital flows become vividly clear. Here is how the sectors are driving or dragging benchmark performance heading into the end of May:

The Alpha Generators (Outperforming the Benchmark)

These sectors are actively pulling the index higher and providing structural outperformance.

Banks and Insurers: The heaviest absolute alpha drivers of late May. Both sectors violently broke away from tracking the index (Neutral) to establish a dominant, Strong relative footing across the Base, Mid, and Short Term horizons. Institutional capital is aggressively overweighting these sectors relative to the broader market.

Diversified Miners: The persistent relative engine. Despite extreme, Overbought spreads against the Top 40 in the Base and Mid Term, it continues to act as a relative leadership block, closing out the month with Strong Short-Term outperformance.

Chemicals: A rigid relative leader. It maintained a High Bullish Base Term spread against the Top 40 throughout the month's volatility, successfully realigning its shorter horizons to a Strong outperformance state.

Telecoms: Providing reliable, low-volatility relative strength. It consistently beat the benchmark on a Base and Mid-Term basis (Strong), offering excellent defensive alpha.

The Alpha Reversals (Losing to the Benchmark)

These sectors previously provided relative strength but have suffered severe institutional distribution, now acting as dead weight or active drags against the Top 40.

Gold Miners and Platinum Miners: The most destructive relative reversals of the month. Both completely surrendered their Strong Base Term outperformance profiles. By late May, they collapsed into a Neutral Base Term spread (merely matching the index) while actively underperforming (Weak) on the shorter-term horizons.

The Tactical Outperformers (Emerging Relative Strength)

These sectors are attempting to close their historical underperformance gaps against the benchmark.

Consumer Staples: Generating aggressive tactical alpha. Despite historically lagging the market (Weak Base Term), it successfully built and maintained a Strong relative bid in the Mid and Short Term, actively clawing back ground against the Top 40.

Luxury Goods: Sustaining a Strong Mid-Term relative advantage, successfully defending its mid-month breakout to drag its Base Term spread up to Neutral (market-performing).

The Benchmark Drags (Chronic Underperformers)

These sectors are the primary source of relative capital destruction, consistently bleeding alpha against the Top 40 index.

Consumer Discretionary: The heaviest anchor on the board. It spent the entirety of May trapped in an Oversold relative Base Term. Holding this sector guarantees severe underperformance against the benchmark.

Paper & Pulp and Technology: Both remain persistent relative laggards. They are pinned under structurally Oversold or High Bearish Base Term regimes against the index, entirely bypassed by the rotational bids lifting the rest of the market.

Hospitals: Attempted a late-month relative bounce, but its underlying structural spread remains a massive headwind (Weak Base Term, Neutral Mid Term), cementing it as a persistent benchmark drag.

Lester Davids

Senior Investment Analyst: Unum Capital

Comments